The economic impact of climate change is becoming increasingly alarming as new studies reveal projections that suggest drastic ramifications for global GDP. As temperatures rise, we face not only a current crisis but a future undermined by a projected 12 percent decline in gross domestic product for each additional degree of warming. This economic toll, described as ‘six times larger than previous estimates,’ underscores the urgency for robust environmental economic analysis and informed policy decisions. Furthermore, the cost of decarbonization efforts must be weighed against potential productivity losses, hinting at a complex interaction between climate policies and economic sustainability. As climate change continues to reshape our world, understanding its economic repercussions will be critical for ensuring future prosperity.

The financial consequences of global warming pose a serious challenge to economic stability and growth prospects. As researchers reevaluate climate change economic projections, it becomes evident that rising temperatures have profound implications for national economies. Particularly, the adverse effects on labor productivity and consumption demand attention as we consider how to adapt to these challenges. Exploring the interconnectedness of climate disruptions and economic viability reveals a landscape where strategic investments in sustainability could mitigate damage. Essentially, grasping the scope of climate change’s productivity effects is essential for creating resilient economies prepared for the realities of a warming planet.

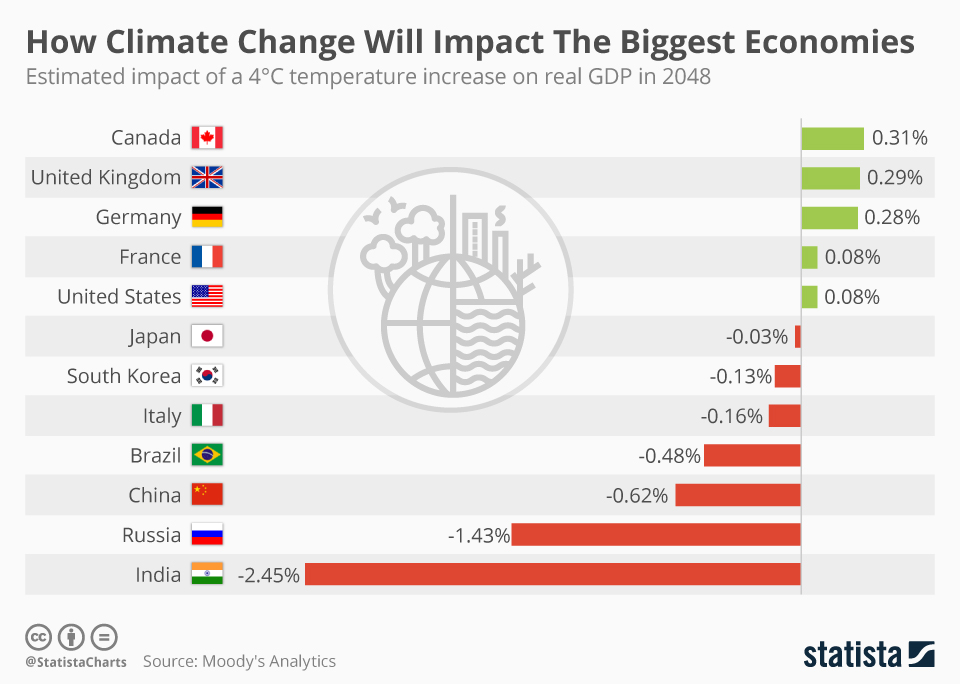

The Economic Impact of Climate Change

The economic impact of climate change is escalating rapidly, as new studies reveal that rising global temperatures can lead to a staggering 12% reduction in GDP for each additional degree of warming. This projection highlights the profound potential losses in economic productivity, reflecting not just immediate costs but long-term consequences on growth. As extreme weather events become more frequent and severe, businesses will face increasing challenges, from disrupted supply chains to rising operational costs, ultimately eroding their profitability.

Moreover, the interconnectedness of global economies means that the effects of climate change will not be confined to the hardest-hit regions. Countries dependent on agriculture, tourism, and natural resources will suffer first, but their downturn will also have ripple effects, leading to a broader GDP decline globally. Macro economic models now suggest that unless significant interventions are made to reduce carbon emissions, we could face a future where climate change-induced economic challenges outweigh any benefits derived from technological advancements and growth.

Climate Change Economic Projections: A New Perspective

Recent analyses of climate change economic projections reveal that previous estimates significantly underestimated the potential economic toll of rising global temperatures. Traditionally, macroeconomists have adopted conservative models, forecasting only modest declines in productivity and spending; however, new methodologies suggest that the reality is much more severe. The research conducted by Adrien Bilal and Diego R. Känzig indicates that the economic fallout from climate change could be six times larger than earlier assessments, prompting a necessary reevaluation of how economic consequences are modeled.

Understanding the economic ramifications of climate change requires a nuanced approach that considers not just localized temperature increases but also global weather patterns. By leveraging comprehensive datasets encompassing over a century of weather and economic data, the authors project that countries heavily impacted by increased temperatures could face not just temporary economic setbacks, but profound long-term challenges to GDP growth, challenging the traditional views held by macroeconomists.

The Cost of Decarbonization: A Necessity for Economic Stability

As discussions around climate change intensify, the cost of decarbonization has emerged as a pivotal consideration for future economic stability. Current projections suggest that the social cost of carbon emissions is significantly higher than previously estimated, with the latest figures indicating a burden of $1,056 per ton globally. This figure starkly contrasts with the estimated costs associated with federal decarbonization measures, highlighting a potential discrepancy in policymaking that could impact economic planning and growth.

Investment in decarbonization is not merely a cost; it represents an essential strategy to mitigate the long-term economic impacts of climate change. By implementing robust climate policies, governments can create economic frameworks that promote sustainable growth while maximizing environmental benefits. The analysis suggesting that decarbonization can pass cost-benefit evaluations even for large economies like the U.S. and the EU reinforces the argument that proactive climate strategy is an investment in future economic health.

Climate Change and Productivity: Assessing the Effects

The effects of climate change on productivity are becoming increasingly evident, with new research indicating that each incremental rise in global temperatures corresponds to a measurable decline in workplace efficiency and output. This phenomenon is particularly evident in sectors heavily reliant on stable weather patterns, such as agriculture and manufacturing. As temperatures rise, the frequency of extreme weather events can disrupt operations, leading to decreased productivity and increased costs for businesses.

Moreover, the link between rising temperatures and decreased productivity levels is not limited to direct impacts; the secondary effects, such as increased health-related absenteeism and diminished workforce morale due to adverse weather conditions, further compound the issue. Companies and governments must, therefore, reconsider their future workforce strategies in the context of a warming planet, specifically how to adapt work environments and maintain productivity in an era of climate uncertainty.

Mitigating Economic Risks Associated with Climate Change

Mitigating the economic risks associated with climate change requires a comprehensive understanding of both environmental and economic factors. Policymakers must collaborate with economists to devise strategies that effectively address the looming threats posed by climate change. This involves not only crafting laws that reduce carbon emissions but also establishing frameworks that support sustainable economic development. Identifying key vulnerable sectors and implementing targeted support measures could mitigate potential losses and foster resilience.

Furthermore, innovative financial instruments, such as green bonds or carbon credits, can play a crucial role in managing the economic risks linked to climate change. By incentivizing investments in sustainable practices, these mechanisms can help transition economies toward a greener future while safeguarding against the financial repercussions of climate-related disruptions. In this way, not only the environment but also the economy can benefit from strategic climate action.

The Interplay Between Climate Policy and Economic Growth

The interplay between climate policy and economic growth is a complex dynamic that requires careful consideration and strategic planning. Traditional views often suggest that stringent environmental regulations could hinder economic progress; however, recent studies challenge this notion by illustrating that sound climate policies can stimulate economic innovation and create new job opportunities. By investing in green technologies and sustainable practices, economies can position themselves as leaders in the emerging global market for clean energy.

Additionally, implementing effective climate policies can lead to substantial cost savings in the long run. Companies that adapt to eco-friendly practices often find that they reduce operational expenses through increased efficiency and minimized waste. As a result, regular investment in sustainable initiatives becomes not just environmentally responsible but also economically advantageous, reinforcing the necessity of integrating climate considerations into broader economic planning.

Understanding Long-Term Economic Outcomes of Climate Change

Understanding the long-term economic outcomes of climate change is critical for informed decision-making and policy formulation. Preliminary data suggests that the economic repercussions of climate inaction could lead to a future where the global economy is significantly stunted. Projections indicate that if temperatures were to rise by more than 2°C, there could be a devastating reduction in global output by approximately 50%—this stark reality suggests that addressing climate change is essential to preserving economic viability.

Furthermore, economic analyses now routinely incorporate multiple scenarios that depict not just the immediate impacts of rising temperatures but also the extensive, cascading effects across sectors and regions. By utilizing advanced climate models that consider both direct and indirect implications, economists can better envision the wide-ranging effects of climate change, making it clear that combating climate change is an urgent and necessary endeavor for the sake of future economic health.

Global Collaboration on Climate Change Mitigation

Global collaboration is paramount in addressing the multifaceted challenges posed by climate change. As repercussions of environmental degradation continue to escalate, nations are increasingly realizing that collective action is essential for effective climate mitigation. This collaboration can take various forms, including international agreements, shared technological advancements, and joint funding for renewable energy projects. Such partnerships can enhance resilience against climate impacts, while also opening new economic pathways through the development of sustainable industries.

Moreover, by pooling resources and expertise, countries can better share knowledge on successful climate policies, leading to more effective implementation worldwide. This global approach not only helps in addressing the immediate threats of climate change but also creates opportunities for international economic collaboration, further highlighting the interconnectedness of environmental health and economic stability in our increasingly globalized world.

Shifting Economic Paradigms in Response to Climate Challenges

As the effects of climate change become more pronounced, there is an urgent need to shift economic paradigms to better reflect the realities brought on by environmental changes. Traditional economic models often fail to account for the broader impacts of climate disruption, such as increased health care costs from heat-related illnesses or the long-term economic consequences of biodiversity loss. As awareness grows, economists and policymakers must develop frameworks that incorporate these climate risks into their analyses and projections.

Embracing this shift is essential not only for effective climate action but also for ensuring sustainable economic prosperity in the future. By incorporating climate resilience into economic planning, nations can develop strategies that not only mitigate the adverse effects of climate change but also harness the opportunities presented by a green transition. This evolving economic paradigm emphasizes the importance of sustainability as a driver of economic growth rather than an obstacle, marking a pivotal change in how we approach economic development.

Frequently Asked Questions

What are the economic impacts of climate change on GDP projections?

Recent studies indicate that climate change significantly affects GDP projections, with an increase of 1°C in global temperatures leading to a projected 12% decline in global GDP. This alarming forecast highlights the urgency of addressing climate change to avert substantial economic losses.

How does climate change lead to a decline in productivity and economic growth?

Climate change can lead to declines in productivity through increased extreme weather events and adverse conditions that disrupt labor, capital, and supply chains. These disruptions negatively impact economic growth, suggesting that the economic impact of climate change could be more severe than previously estimated.

What are the costs associated with the decarbonization process in relation to climate change economic projections?

The cost of decarbonization is crucial in evaluating climate change economic projections. Recent analysis indicates a social cost of carbon between $185 to $1,056 per ton, emphasizing that while decarbonization incurs costs, it is economically beneficial compared to the substantial GDP losses projected due to climate change.

What are the long-term economic impacts of a 2°C increase in global temperatures?

A long-term increase of 2°C in global temperatures could lead to a staggering 50% reduction in output and consumption, which would be twice as severe as the Great Depression. This highlights the severe economic ramifications of climate change if significant measures aren’t implemented.

How does environmental economic analysis inform us about climate change and its economic toll?

Environmental economic analysis helps us quantify the economic impact of climate change by examining how temperature increases correlate with GDP decline and productivity losses. These analyses provide critical insights for policymakers to address and mitigate the future economic toll of climate change.

What is the relationship between climate change and extreme weather events in economic terms?

The relationship between climate change and extreme weather events is significant, as rising global temperatures contribute to more frequent and severe weather phenomena. These events disrupt economic activities and infrastructure, leading to substantial economic costs and losses, further complicating climate change economic projections.

| Key Points |

|---|

| The economic impact of climate change is more severe than previously estimated. |

| A recent study found each 1°C increase results in a 12% decline in global GDP. |

| Losses peak six years after the temperature rise is recorded. |

| Previous macroeconomic models underestimated the severity of climate change’s economic toll. |

| Decarbonization policies are economically beneficial for major economies. |

| Failure to address climate change could lead to a 50% reduction in output by 2100. |

| The social cost of carbon is significantly higher than previously estimated. |

Summary

The economic impact of climate change is profound and alarming, with recent studies projecting that rising global temperatures could severely diminish GDP on a global scale. As temperatures increase, the economic consequences could be six times larger than previous estimates, culminating in drastic reductions in productivity and consumption. With each degree of warming, we face the possibility of significant, long-lasting economic losses, emphasizing the urgency for effective decarbonization strategies. These measures not only align with environmental goals but also prove advantageous from an economic standpoint, highlighting the need for immediate action against climate change.