The commercial real estate crisis is emerging as a pressing concern for economists and investors alike, as high office vacancy rates threaten to destabilize the market and the broader economy. Following the pandemic, many businesses have shifted to remote or hybrid work arrangements, leading to an alarming decline in demand for downtown office spaces, where vacancy rates hover between 12% and 23% in major cities like Boston. With a significant portion of real estate loans coming due by 2025, financial experts warn of potential bank failures—especially among smaller banks that may struggle to absorb losses from these troubled assets. Compounding the issue, the Federal Reserve’s reluctance to lower interest rates means that refinancing options remain constrained, prompting fears about the economic impact if delinquencies rise. This situation raises urgent questions about the future of commercial real estate and its potential ripple effects on the entire U.S. financial system, highlighting a critical juncture in the intersection of work, economy, and real estate finance.

As we delve into the current situation within the commercial property sector, it’s essential to acknowledge the implications of the ongoing real estate downturn, often referred to as a crisis in the commercial property market. With many office buildings standing empty and a notable drop in occupancy rates, the repercussions are evident—a surge of banks facing challenges tied to real estate investments. Simultaneously, the tightening of lending due to bank distress could curtail overall economic expansion, stirring concerns of a domino effect not experienced since previous financial downturns. Furthermore, with looming deadlines for substantial commercial mortgages, the landscape is rife with uncertainty, prompting discussions about the viability of various financial institutions. Understanding this complex interplay of factors is crucial for gauging the future trajectory of both commercial real estate and economic stability.

Understanding the Commercial Real Estate Crisis

The ongoing commercial real estate crisis stems from a confluence of factors that have starkly altered the landscape of office space demand. In the aftermath of the pandemic, high office vacancy rates have persisted, with major U.S. cities witnessing rates between 12 to 23 percent. This significant decline in demand has led to a depreciation in property values across the board. As businesses reassess the need for office space, many buildings remain empty, exacerbating the financial strain on commercial real estate investments.

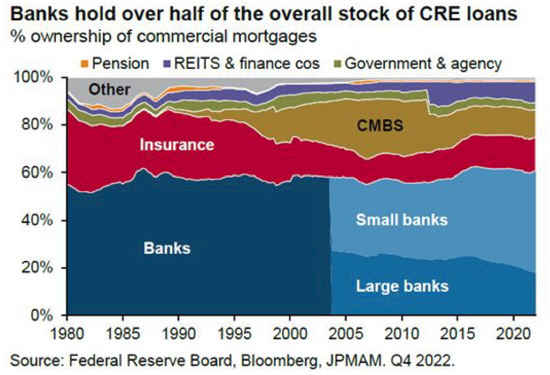

Moreover, the surge in commercial real estate loans set to mature by 2025 poses a considerable risk to financial institutions. With about 20 percent of the $4.7 trillion commercial mortgage debt coming due this year, banks, particularly smaller ones with lighter regulatory oversight, could face severe consequences. If delinquencies rise among borrowers unable to navigate the high vacancy environment, the subsequent wave of defaults could trigger a ripple effect, destabilizing not just banks but the broader economy.

Frequently Asked Questions

What is the current state of the commercial real estate crisis in relation to bank failures?

The commercial real estate crisis is deeply intertwined with potential bank failures as high office vacancy rates have led to significant losses for lenders. As many commercial real estate loans reach maturity, banks may face difficulties, particularly smaller institutions that have less stringent regulations. While large banks appear stable, the ripple effects of delinquent loans could still impact the wider banking system.

How does the high office vacancy rate contribute to the commercial real estate crisis?

High office vacancy rates, which currently range from 12% to 23% in major U.S. cities, have resulted from a shift to remote work post-pandemic. This decline in demand has depressed property values and increased the risk for banks holding commercial real estate loans, exacerbating the commercial real estate crisis as more investors face losses.

What economic impact can we expect from the unfolding commercial real estate crisis?

The commercial real estate crisis is likely to have significant economic impacts, particularly through distress in regional banks, which could lead to tighter lending conditions and lower consumer spending. However, this occurs in the context of a strong job market and stock market, which may soften the blow in the short term.

Are rising Federal Reserve interest rates worsening the commercial real estate crisis?

Yes, rising Federal Reserve interest rates are contributing to the commercial real estate crisis by increasing borrowing costs and making refinancing more difficult for those with existing loans. This situation is compounded by the high office vacancy rates and an overall decline in demand for commercial properties.

What can be done to mitigate the effects of the commercial real estate crisis?

To mitigate the commercial real estate crisis, a drop in long-term interest rates could help facilitate refinancing for struggling properties. However, significant bankruptcies in the sector may also be necessary as part of market corrections, as bankruptcy is a common occurrence in the real estate business.

Will the commercial real estate crisis lead to a full-blown economic downturn?

While the commercial real estate crisis poses risks to the economy, including potential distress among banks, experts argue it is not likely to trigger a full-blown economic downturn like the one experienced in 2008-2009. Financial regulations post-2008 have helped large banks weather shocks better than in previous crises.

What demographic factors are influencing the commercial real estate crisis?

Demographic shifts, particularly the rise of remote work and changing commuter patterns, have greatly influenced the commercial real estate crisis. In the U.S., many workers continue to favor remote work, leading to decreased occupancy rates in office spaces and contributing to the broader downturn in the market.

How might regional banks be affected by the commercial real estate crisis?

Regional banks, which have invested heavily in commercial real estate, may face severe impacts due to high delinquencies on loans. Given their lesser capital requirements compared to larger banks, regional banks are particularly vulnerable and could struggle if significant losses arise from the commercial real estate crisis.

| Key Point | Details |

|---|---|

| High Vacancy Rates | Vacancy rates for office spaces in major U.S. cities range from 12% to 23% since the pandemic. |

| Risks of Bank Losses | 20% of the $4.7 trillion in commercial mortgage debt is due this year, potentially causing significant losses. |

| Impact on Economy | While some banks may face losses, a full-blown financial crisis is not expected. The economy is still relatively strong. |

| Factors Contributing to Crisis | Over-leveraging, rising interest rates, and a drop in demand for office spaces contribute to the crisis. |

| Potential Solutions | A reduction in long-term interest rates would help, but this is viewed as unlikely without a severe recession. |

| Regional Banks at Risk | Smaller banks, having invested heavily in commercial real estate, are more vulnerable to market fluctuations. |

| Long-Term Outlook | The outlook for commercial real estate remains cautious, with some investors hopeful for interest rate drops by 2025. |

Summary

The commercial real estate crisis is a significant concern as high office-vacancy rates could have serious repercussions for the economy this year. With rising interest rates leading to a surge in delinquencies on commercial property loans, the financial stability of many banks is under threat. Although widespread bank failures are not anticipated, the effects of these challenges could ripple through the financial system, impacting not just commercial real estate investments but also consumer confidence and economic activity. As we monitor the situation, it’s essential for stakeholders to stay informed and proactive in addressing the underlying issues within the sector.